Is Competition Still for Losers?

The competitive landscape is changing, how should you respond?

Welcome to all the new subscribers who have joined us over the last week! If you haven’t already, you should check out my last article here:

If you like what you read, please subscribe to Superfluid here:

This week, one of my close friend’s launched a new mini-OS for iPhones that makes your smartphone dumb!

It’s awesome to finally see it live, having seen all the effort that’s gone into building this from the ground up. Congrats to the Minimis team!! 🎉🎉🎉

As an Android user, I’ve had the privilege of using Minimis over the last year and it’s saved me hours and days from just doomscrolling on my phone. It’s beautifully minimal, super functional and has fun ways of locking away addictive apps!

Every year I make it a point to rewatch Peter Thiel’s famous Stanford lecture “Competition is For Losers”. It’s by far one of the most impactful pieces of startup content that I’ve consumed, and each time I watch it, I always pick up something new.

It is a basic economic theory that perfect competition drives profits toward zero, and monopolies capture lasting value. And whilst it’s really hard to build a true monopoly, it is entirely possible to dominate as a startup in a market and category that you create, which is the ultimate point Thiel is trying to make here.

However, as AI reshapes entire industries, dramatically reframes timelines and changes the urgency and structure of how large incumbents react to being disrupted, is competition still for losers? or does having horizontal and vertical breadth matter more to be able to win the hearts and minds of customers?

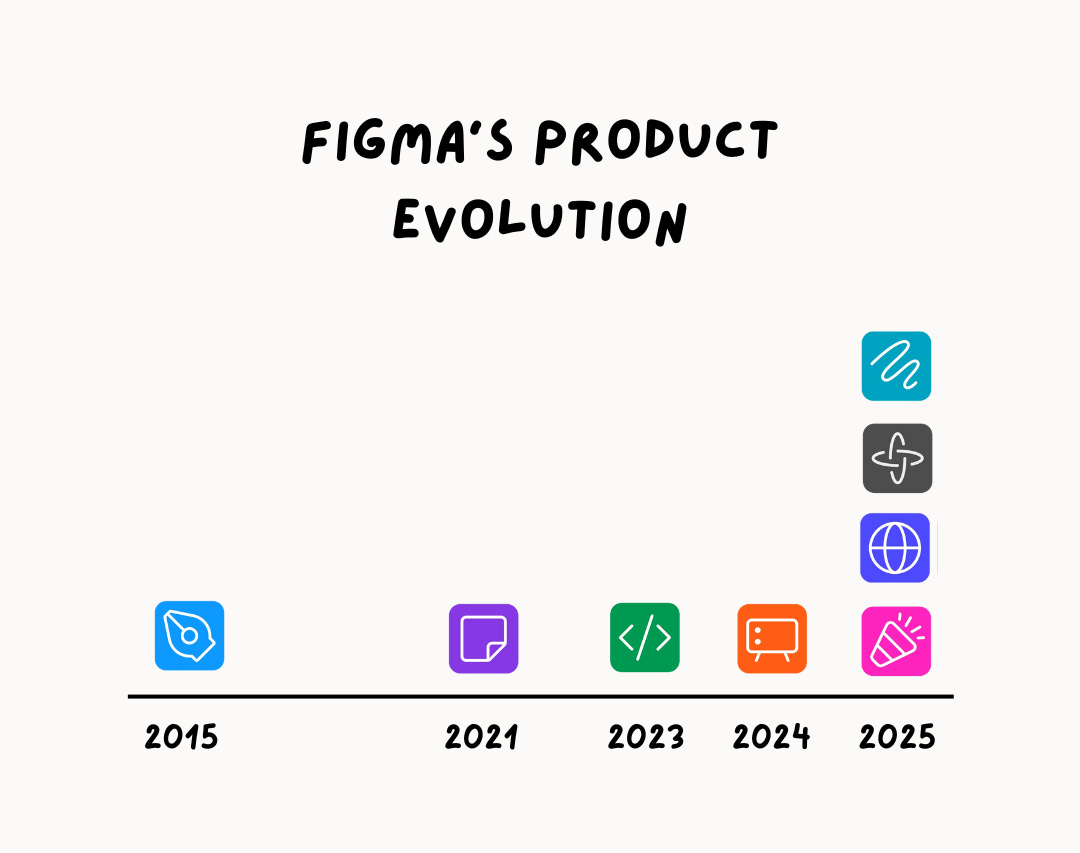

In 2015, Figma was a design tool focused on enabling greater web-based collaboration amongst designers.

In 2025, Figma is now a “system of record for design and product development” and is the perfect case study in how AI enables aggressive product bundling.

From Figma’s recent S-1 filing:

Since then, we have added products and features to support the process of going from idea to product. In 2021, we launched our second product: FigJam, an online whiteboarding tool [...] In 2023, building on years of bringing design and code closer together, we launched Dev Mode, a product tailored for developers [...] In 2024, we introduced Figma Slides to give teams a new tool to drive strategy and alignment along the way.

In 2025, we doubled our product portfolio with the launch of four new products: Figma Sites, Figma Make, Figma Buzz, and Figma Draw [...] In 2024 alone, we shipped 180 new features and updates. Our customers recognise the benefits of the interconnectivity across our platform, with 76% of our customers using two or more products during the three months ended March 31, 2025

It’s interesting to see Figma expand out of its core monopoly and category to compete directly with PowerPoint, Canva, Webflow, Illustrator, and Cursor all at once, in the pursuit of owning the full, end-to-end workflow before one of these other platforms do.

But perhaps this is the rational response to AI-driven competitive dynamics where AI allows you to create more of the same. In the case of Figma, they are fortunate that many of their users aren’t only designers, but also engineers, operators, marketers etc,. and so have a higher chance of expanding revenue through feature sprawl.

However, this feature sprawl highlights a growing trend. Companies are now producing software faster than they can release it, and releasing software faster than users can adopt it.

Initially, it was clear that foundation models would be commoditised and interoperable (which in part is playing out), but now if everyone has the same feature set, does this mean vertical applications get commoditised too?

Not necessarily. This strategy can definitely work, and has certainly worked in the past (in less noisier times). One of the best examples of this is probably the launch of Microsoft Teams. Its success depended on structural advantages that many companies attempting similar strategies fundamentally lack:

Deprecation leverage — Microsoft could strategically sunset Skype for Business, effectively forcing enterprise customers to migrate to Teams. This deprecation control represents a unique form of market power unavailable to most software companies, who must compete for user attention rather than mandate product transitions. This foundational advantage enabled the other two strategic benefits.

Existing distribution — Microsoft possessed unparalleled distribution reach through Office 365, automatically placing Teams in front of hundreds of millions of enterprise users without requiring separate acquisition efforts. This eliminated the customer acquisition cost that typically makes bundling strategies economically challenging.

Switching costs — Enterprise customers had already invested heavily in Microsoft's productivity ecosystem, with Teams integration creating additional switching friction. The cost of migrating away from Teams wasn't just the communication tool itself, but the entire interconnected Office workflow that enterprises had built around Microsoft's platform.

These structural advantages created a bundling environment fundamentally different from the AI-driven expansion strategies we observe today.

Most companies pursuing AI bundling strategies have strong market power in their vertical, but lack this on a horizontal level and face the challenge of proving value for each new feature while competing against focused specialists who can deliver superior solutions within specific categories. For example, we literally have 100s of startups going after the holy grail of building the best AI coding agent in the world, alongside 5+ incumbents.

We’ve never seen this level of overlapping competition before and in terms of capital deployed and money incinerated, it makes the Uber vs Lyft battle look like child’s play by comparison.

And so, if you’re competing head on with anyone (startup or incumbent), competition is more for losers than ever before. It’s tough to build a strong distribution advantage in spaces that are rapidly commoditising, creating a perfect competition dynamic where profits asymptote towards zero.

Moreover, creating categories is also harder today than it was maybe a year ago. There are so many niche applications that exist, and so many variations and remixes of software and tools that defining your category, and subsequently educating users about it is incredibly hard (hence why capturing attention is key).

For startups, this creates a particularly challenging environment. The traditional advantages of speed and focus become less meaningful when incumbents can match startup velocity while maintaining their structural advantages.

So what does that actually mean?

The path to avoiding competition has changed, and simple category creation isn't enough to build a durable business. It is imperative that a startup looks to redefine and reinvent the game entirely.

This leads to two strategic imperatives for AI-era startups:

Master Counter-Positioning. At the moment, it feels like most AI startups are improving individual parts of a workflow, or are helping people automate steps 1 to 3, with a manual handoff for step 4 and 5, and sure, this is valuable, but it isn’t durable. Incremental improvement is important, but now, easily duplicated.

Instead, your job is to discover previously impossible ways of operating, build a product that addresses this and then convince the market that your new approach is both right and easier than what they're doing now. Open-ended software (especially with in-built AI) is overwhelming. Constraint and opinionated workflows that deliver better end to end results are key.

Build Process Power. When feature parity is possible in weeks and months rather than years, durable competitive advantage comes from organisational velocity and the way your team uniquely creates value for your customers. This isn’t about have the most cracked engineers, or highly optimised processes or talented sales people, but its about building an organisational engine that can learn, build, and iterate faster than anyone else can match.

Calvin French-Owen’s reflections on OpenAI article that dropped this week provides a very practical and candid example of this. In summary, OpenAI’s organisational structure (or lack thereof) makes it easier to pull people in from different teams to sprint quickly at a feature release that is showing internal promise. The ability to build conviction, corral resources and fully commit at launching something worthwhile is very unique and probably down to the company’s meritocratic ethos.

This is something that can’t be bought, or rushed. It’s cultivated over time through culture, talent density and competitiveness.

The opportunity for founders who internalise this and are able to get this right is unprecedented. While everyone else is trapped in games of margin compression and aiming for feature parity, companies that do something entirely different and reinvent the game being played will be rewarded greatly.

Competition is certainly still for losers.

Make sure to subscribe now to not miss next week’s article

How did you like today’s article? Your feedback helps me make this amazing.

Thanks for reading and see you next time!

Abhi