Why Fundraising is Easy for Some and Hard for Others

A quick formula breaking down the basics of fundraising and why you might be finding it hard

Welcome to all the new subscribers that have joined us over the last week! If you haven’t already, you should check out my last article here:

If you like what you read, please subscribe to Superfluid here:

When I talk to first-time founders currently raising a round, their most common frustration is how challenging fundraising is for them compared to how effortless it seems for others raising similar or larger amounts.

Sometimes it's hard to explain the complexities and nuances between different investment opportunities fully. Moreover, some aspects of why fundraising is easier for some companies versus others aren't necessarily controllable for a founder, making it even harder to grasp.

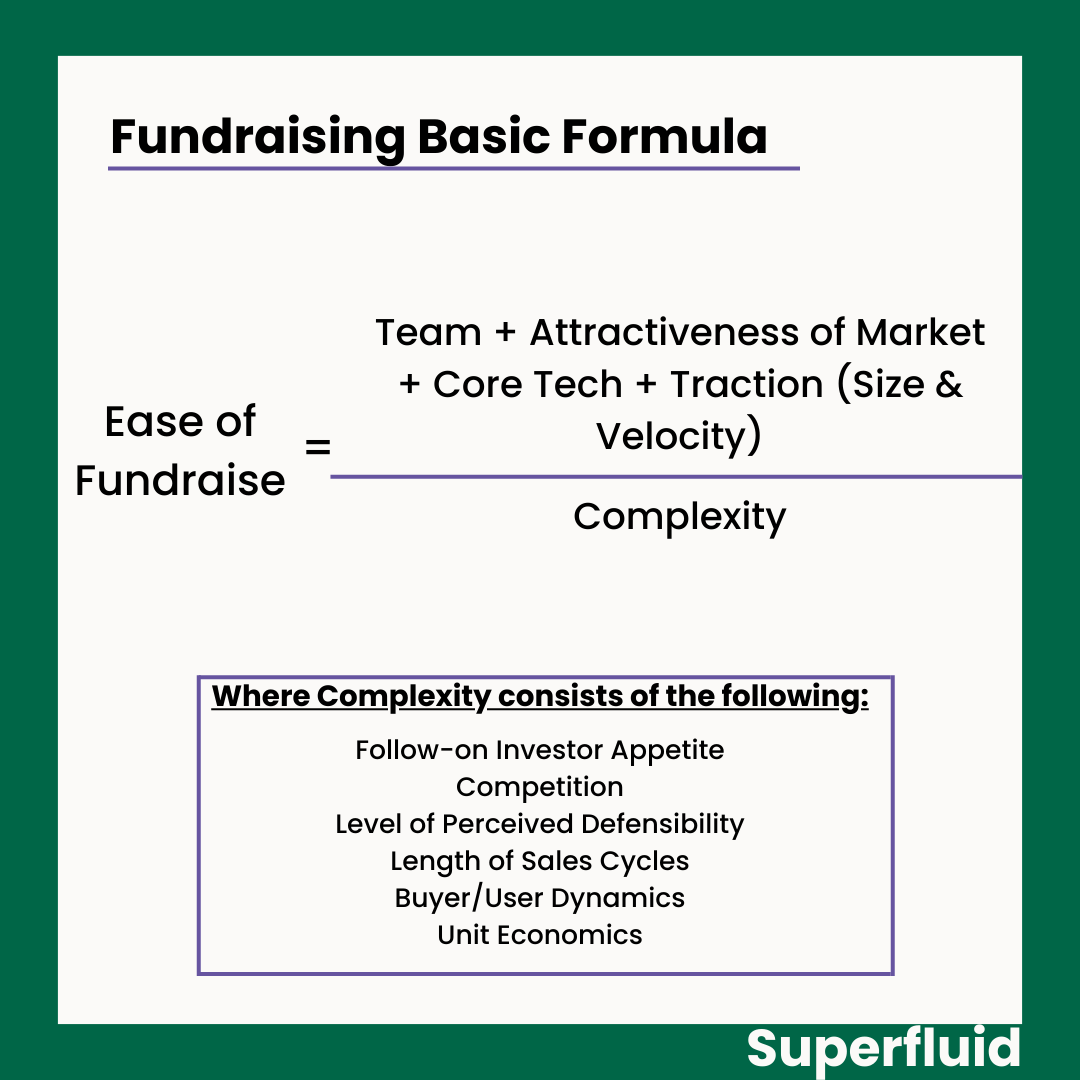

As such, I've tried to distil this into a basic formula:

I’ve constructed the formula, where the numerator consists of factors that positively contribute to the ease of fundraising if there is a particular spike in any of these categories. If there is no spike, then these factors may hinder fundraising efforts.

Team: This one is easy. The more experienced and seasoned the founding team is, the easier it is to raise capital as people can trust in the team's ability to build a valuable business. However, there is nuance here where all experience is not necessarily good experience.

Core Tech: Some people might think this is product, but I like to think of it as the core technology your product is built on. For example, this might be Crypto or AI in recent times. It might relate to breakthroughs in Quantum or Nuclear tech if we're thinking about deep tech startups. If you're harnessing the latest technology and building alongside a recent breakthrough, investors will be more receptive and will try to time/move ahead of the hype cycle.

Attractiveness of Market: The core tenet of early-stage investing is to back strong founders building in strong markets at the right time. The size, growth potential and sentiment towards your particular market (e.g., construction, HR teams, government) will also strongly dictate how easy it is to raise a round.

Traction (Size and Velocity): Both size and velocity of growth are important to investors. Fast growth shows that there is pent-up demand for the product, even if the actual revenue number isn't large yet. On the flip side, if you've made $1M but taken perhaps 12 months to get there, that's also okay, provided there is a pathway to greater scale and velocity.

I don't necessarily think any of the parts of the numerator are controversial or that surprising. It's pretty standard stuff that VCs look for, which I think most founders understand.

I’ve left the denominator as a general term ‘Complexity’ because it really breaks down into a multitude of factors with subjective levels of influence over the complexity of investing in a certain business.

The further nuance to understand is really figuring out what founders can or can’t control. The list below is ordered from uncontrollable to controllable from a founder's perspective.

Follow-on Investor Appetite: The large bulk of the early-stage VC market is geared towards optimising for later-stage investor appetite. Small pre-seed and seed funds are entirely reliant on later-stage investors to invest in their portfolio companies in 18-24 months. However, this means that it's hard to know what type of company will be in demand in the future. This is largely uncontrollable from a founder's perspective.

Competition: If you are building in an area with a vast array of competitors (either direct or adjacent), this will almost certainly count against you in some way. While you can’t control the number of competitors that exist, you can control the way you go about building your product, crafting your business model, or structuring your team to stand out amongst these competitors.

Length of Sales Cycles: VCs love scale and velocity. If your sales cycles are long, you need to ensure that you’re making that up with large ACV contracts. If not, you’re undoubtedly going to get penalised for it with extra scrutiny during DD.

Buyer/User Dynamics: On the GTM side of the business is figuring out the relationship between the buyer and the user. If the buyer of the product isn’t the user, then it becomes tricky to get super comfortable that in the early days of the product that engagement and use of the product will be high. You’ll need to show more user traction metrics to work past this objection.

Level of Perceived Defensibility: Especially now when AI is the hottest core technology you could use to build, having a high level of perceived defensibility is key. The nuance here is around the word ‘perceived’. Whilst you might think your business is defensible for a myriad of reasons, none of that matters if investors or VCs don’t believe them. Not enough founders seem to think overly hard about whether their business is defensible now, or the path to building a defensible business over time.

To note, the list of complexities above is definitely not exhaustive. Some investors will have subjective opinions about other factors of your business that will make it harder to raise from them. But on the whole, the five factors above are typically the common reasons for why a pre-seed business struggles to get funded.

As a founder, you should recognise and address the factors you can control, or think through the possible solutions to these objections. For example, suppose you believe there is less appetite from later-stage investors for your type of business. In that case, it’s important to think through how you can craft a future for your business where you’ve only raised one round of funding and self-sustained from there to build a large revenue-generating business.

Even if the factors seem uncontrollable, or you think that VC’s just don’t ‘get it’, I think the best founders are able to force through the objections a VC might have and make them look at the positives for the business.

Make sure to subscribe now to not miss next week’s article

How did you like today’s article? Your feedback helps me make this amazing.

Thanks for reading and see you next time!

Abhi