A Strategic Guide to Sequencing Your Fundraise

Increase the probability of success when raising capital with this simple technique

Welcome to all the new subscribers that have joined us over the last week! If you haven’t already, you should check out my last article here:

If you like what you read, please subscribe to Superfluid here:

It's no secret that Pre-Seed and Seed startup fundraising is all about getting at least 1 person to believe in you.

As a result, a lot of founders take a wide market approach towards fundraising. They reach out to every single investor they know, hunt for warm intros to investors that they don't know and fill out countless website pitch forms for funds they haven't ever heard of.

If that's your approach to fundraising, you're going to get exhausted real quick. Filling your calendar back to back for 10 hours a day isn't an achievement, it's stupidity.

Instead, I'd encourage you to treat the fundraising process like a product. You need to do the work to learn and iterate and make sure you can deliver a stellar product (i.e., pitch) when it matters.

In this article, I'll give you the only guide you need to sequence your fundraise, and a template investor CRM that'll help you manage the entire process from start to finish.

Sequencing Your Capital Raise

Fundraising is effectively the same as running a sales process, except you're selling to investors. The goal of this guide is to increase the probability of success in securing investment. Everyone’s fundraising journey is different.

Step 1:

The first step to fundraising is compiling a list of investors that you want to target. The easiest way to do this is by getting a temporary Crunchbase subscription and downloading lists of all active investors based on the following criteria:

Your stage

Your geography (e.g., US, Europe, Asia, Australia etc)

Your industry/market

A lot of founders go wrong at this point. They fill their list with literally every investor in the world and think that everyone will be interested in their business. Instead, it's important to know what the investment mandate is for each fund and check whether you meet the baseline requirements.

For example, if you're the founder of a B2B SaaS business based in Europe, you definitely shouldn't be reaching out to investors who only focus on Australian consumer businesses.

It's important to keep this list to a manageable amount. Anywhere from 50 - 100 investors feels about right.

Step 2:

Using your list of investors, I want you to rank/prioritise them according to the following tiers:

Tier 1: These are your most preferred investors. They could be brand name firms, sector specialists or high value-adding angels. You would do anything to get these investors on your cap table

Tier 2: These are investors you kind of care about and would still want on your cap table but aren't your first choice.

Tier 3: These are your backup investors. They are your safety net if anything goes wrong with investors in the first two tiers

Tier 4: These are your practice investors. They're funds that you don't really care about because it's unlikely they'll add value to your business, or be a constructive partner at the early stage.

With this step, it's important that you're ruthless.

A lot of founders will be scared of writing off investors before even pitching them, but the entire point of fundraising is finding people who will believe in you and will actively help you grow a big business without hindering it. You should be selective about who you want on your cap table (see my article on this here).

Step 3:

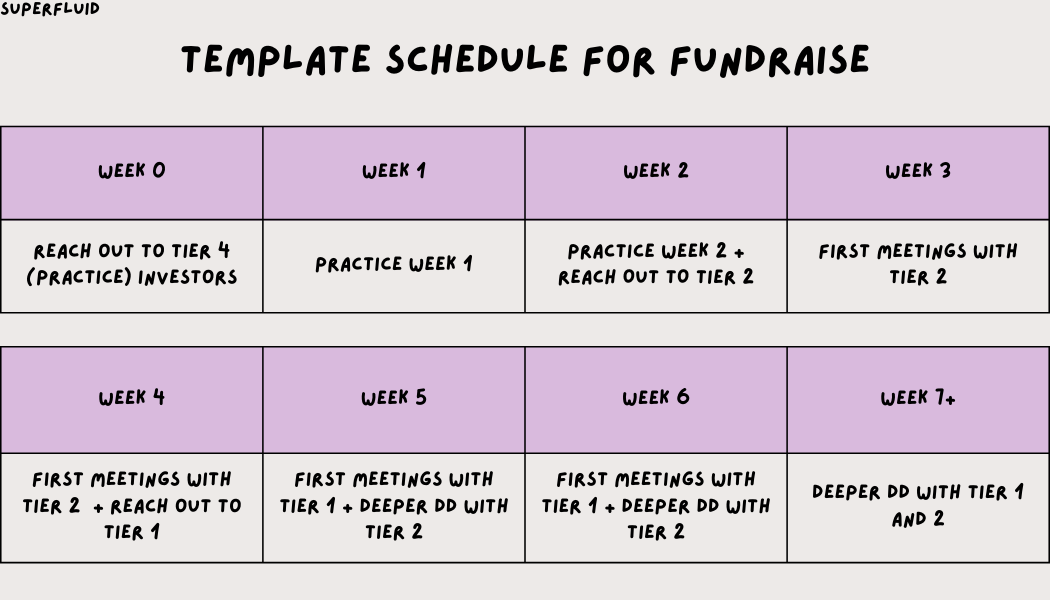

Once you've ranked the investors on the list, the next is to create a schedule.

Let's say it takes about 6 - 8 weeks to get to a term sheet.

Breaking that down, I think your schedule for the first 7 weeks should follow something like this:

Now the weeks don’t necessarily matter so much, but the sequencing does. It’s important that you take two weeks to practice your pitch with investors who don’t really matter that much to you.

This is the most crucial step of the process as it will set you up for success with later conversations. Initially, most VCs will probably have the same questions about your business. Once you go into deeper DD, the individual risks that a particular VC anchors to will become apparent and the questions will be more bespoke.

Step 4:

The next step is figuring out how to get meetings with investors.

The easiest way is through warm intros. You can source these from other founders, angel investors or startup operators.

The other way is through cold emailing, or filling out a pitch form on the fund’s website. Some investors are really good with this and will respond to everyone who comes in cold, others neglect this channel completely.

Step 5:

Once investors start responding to you, my suggestion is to book at least 4-5 pitches a day with at least a 30-45-minute break between each pitch. Pitching is your full-time job for the next period of time. It’s going to be annoying and distracting from building your business, but my view is if you are methodical and go hard at it, you’ll be able to wrap it quicker than if you were to run a drawn-out process.

Step 6:

It’s finally pitching time!

Make sure that you’re joined by someone else on each call. Ideally, this is your co-founder(s), but could also be an early employee.

This person’s role is to take notes and watch how the conversation unfolds. It’s important for this person to accurately capture the questions asked, and the VCs reaction when an answer is given. If you don’t have a second person to join you, then you’ll need to figure out how to multi-task whilst answering questions.

Iterating On Your Pitch

In addition to taking notes and capturing the questions asked, throughout the entire process, the onus is on you to flip the script back on the investor and ask them lots of questions. You effectively want to treat them as a customer. Pay specific attention to the terminology they use when answering your questions.

The 4 main areas that I think are important to cover with a VC:

The reasons why they are excited about your business. You’ll be able to tell if they truly believe in you and your vision by how they answer this question. The normal indicators of excitement apply here, e.g., if they talk quickly, or they start brainstorming ways in which they think a deal could work it’s probably a good sign.

Their key objections to your business and why they have those objections. Lots of founders ask VCs why they wouldn’t invest but take the reasons at face value. You need to push hard on this as many VCs will be guarded and not tell you the truth.

What a successful partnership would look like from their perspective. You need to get VCs to explain how they like to work with founders. Get them to sell themselves and pitch why they should be on your cap table. You’ll understand what they value and whether that’s a right fit for you. If they promise they’ll do XYZ for you - interrogate what that actually looks like.

What their investment process looks like. If they like to do lots of DD, then you can be prepared for information requests and plenty of meetings.

Founder Resources

To help you manage the fundraising process, I've created a Fundraising CRM template that you can use through Google Sheets, Excel or Notion.

You can find them here:

Google Sheets: Link here

Notion: Link here

Excel:

This is my first time creating a template for public use, so please let me know what you think! Also, let me know what other templates you’d like me to create in the comments below.

Make sure to subscribe now to not miss next week’s article

How did you like today’s article? Your feedback helps me make this amazing.

Thanks for reading and see you next time!

Abhi

Overall - great high level outline of how to think about fundraising. Reminds me of Paul Graham's notes but with more of a "workbook" style approach. Thanks for sharing.