Why Mega Funds Exist

Unpacking how institutional investors allocate their capital

Welcome to all the new subscribers that have joined us over the last week! If you haven’t already, you should check out my last article here:

If you like what you read, please subscribe to Superfluid here:

Before we get started this week - I have one small request for all of you.

I’d love to ask all of you for feedback on how I can make reading Superfluid a better use of your time.

If you could spare 1 minute of your time, I’d greatly appreciate it.

VCs are just middlemen.

Whilst a select few are rich enough to invest their own money, 99% of VCs raise money from rich people, large institutions and other corporations.

In particular, the backbone of the VC ecosystem is institutional investors such as college endowments, pension funds and large foundations.

VCs have a fiduciary duty to deploy their capital responsibly. However, in recent times, the incentives guiding institutional investors, VCs and the founders that receive investment misaligned.

In this article, we’ll unpack how institutional investors construct their portfolios, make investment decisions and the impact that has on the VC ecosystem.

The Endowment Model

Institutional investors all have different return expectations, risk limits, assets under management and portfolio construction preferences. Some investors might purely invest in funds and others might supplement fund investing with direct investments in startups.

Amongst the largest institutional investors are grant-making endowments and foundations. This means that every year, they must allocate a certain percentage of their portfolio (typically 5%) to grants for their community. These investors also look to make grants in perpetuity, meaning they have low liquidity requirements.

As a result, most of these institutions follow a popular portfolio construction methodology called the Endowment Model developed by the late David Swensen. Swensen spent 36 years managing Yale's Endowment fund and pioneered a focus towards investing in illiquid assets such as Real Estate, Infrastructure, Private Equity and Venture Capital. By doing so, Swensen theorised that the illiquidity of these asset classes should be embraced in line with the Endowment’s low liquidity requirements.

As such, most institutions that adopt the Endowment Model might have around 10-30% of their portfolio allocated towards private, illiquid investments. Out of this, 2-10% could be allocated to Venture Capital.

Over the last 13 years, assets under management grew rapidly for all of these endowments. Either through stellar returns, or large donations, many of these institutions had more money than they knew how to deploy. Obviously, the measly 2-10% allocation to VC also grew in absolute dollar terms resulting in a requirement to deploy large chunks of cash at a quicker pace.

However, deploying capital into private investments is tricky. Fund managers only raise new funds periodically, and aren't capable of taking on an unlimited supply of funds. Moreover, capital is drawn down over time through capital calls, rather than deployed upfront.

This means that institutional investors plan out their prospective commitments usually at the start of the year, with a mid-year review. The goal of this process is to ensure that the portfolio is either at its target allocation or has a line of sight towards getting there.

The planning exercise requires a bit of modelling by taking into account new commitments over the year, capital calls from previous commitments and any distributions/returns that might come back from fund managers. It is in the LPs’ best interest for fund managers to call capital (e.g., quarterly) and raise new funds (e.g., every 2-3 years) at a regular cadence.

Manager Selection

Investing in a VC fund is basically Power Law^2.

VC Funds run on a power law basis, where a small number of investments contribute to the majority of returns.

On top of this, VC fund returns also exhibit a power law distribution. High-performing funds are rare and can easily make up for a bunch of duds.

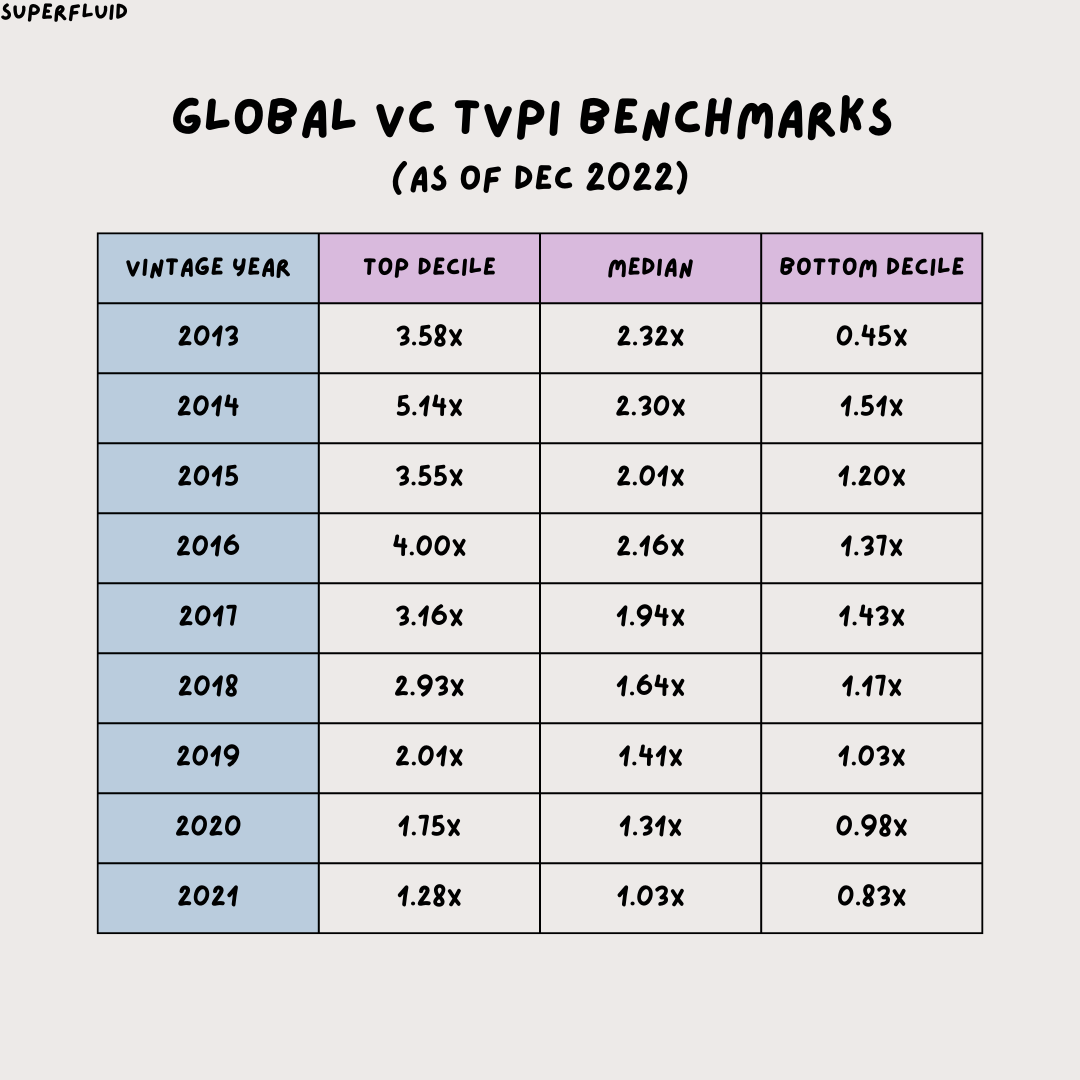

From the table, above, we can look at the distribution of returns from funds in each given vintage. In 2013, the top decile threshold is 3.58x, meaning for every $1 invested, the best 2013 vintage funds, returned at least $3.58 back, if not more. As you can see, the disparity in TVPI between the top decile and the median is quite substantial between 2013 - 2016.

To exploit the power law, VC funds usually invest in 20 - 30+ companies with the expectation that a couple will return the fund. This doesn’t translate to fund investing due to a few incentive misalignments and nuances that exist for institutional investors.

Most employees at an institutional investment fund are not incentivised by outperformance. Many receive a standard salary package and perhaps an annual bonus, but no form of carry or share in the institution’s annual profits. As a result, there is no direct correlation between an employee's ability to pick strong fund managers to their remuneration.

These funds look to maintain their assets under management in line with their grant-making activities and inflation. Thus, their return expectations are usually between 3.5% - 5.5% + CPI. This isn't a hard hurdle to hit, meaning funds don't need to take on extra risk in order to achieve their return target.

As with VCs needing to fight for access to the best deals, institutional investors also need to fight for access to the best fund managers. In many cases, top VCs such as Sequoia and Benchmark already have a full stable of LPs that will continue to invest in future funds. That means access is only available when one of these LPs doesn't invest in the next fund, which is a rare occurrence.

Institutional investors have their own fund concentration limits to abide by. This means that for an institutional investor to invest in a VC fund, their commitment, shouldn't exceed X% of the total VC Fund size. Usually, this limit is 20-30% of a fund. E.g., if VC Fund A is raising a $100M fund, Institutional Investor B can only invest $20-30M in that fund.

Once an institutional investor chooses a fund manager, they will look to invest in multiple funds over a period of time. By investing in funds that start investing in different years, investors hope to get vintage-year diversification. The vintage year for a fund is the year in which it makes its first investment. This is important because fund performance might vary wildly depending on the broader macro climate during its investment period.

As a result, institutional investment portfolios are typically optimised for easy ongoing management and 'lower' risk-taking. That means that it is incredibly hard for new fund managers to receive capital from an institutional investor with an existing private investment portfolio. As the saying goes, "Nobody gets fired for buying IBM".

So how does a VC actually receive investment from an institutional investor?

First and foremost, there needs to be space in the portfolio for a new VC. This typically happens in a few ways

An existing VC manager is underperforming, and the LP decides not to allocate further capital to future funds

The allocation to VC increases, meaning more money needs to be deployed

The LP is early in its VC strategy and is looking for further diversification across strategy/stage/thematic

Once the need for a new VC is recognised, the search process begins. LPs have likely accumulated relationships with numerous VCs already and will look to choose out of their favoured 'bench' managers.

Selecting a fund manager is largely based on these criteria:

The track records and the pedigree of General Partners. If you've worked as a partner at any Tier 1 fund and have some strong unicorns as part of your track record, you won't have much of a problem attracting LPs to your fund

The ability to deploy and return capital. Investors look to see if fund managers can put their money to work quickly and effectively. Distributions also matter but are reliant on the vintages of existing funds. Many emerging VCs may not have been in business long enough to have any exits

How they source investments, win allocation and support their portfolio companies. Each fund manager will have their own take on their competitive advantage and why they think they will perform better than other funds

Whether the fund fits within the LPs venture portfolio. Diversification is key to portfolio construction. Investors won't want portfolio overlap (i.e., two venture funds with similar investment styles, strategies and perhaps even portfolios). In small markets, this becomes even more of a concern

Whether the amount they are raising makes sense and if their strategy scales. Deploying $50M across 20 companies is different to deploying $500M. Understanding the investment parameters of a given fund is important. If you wanted to deploy $500M across 100 portfolio companies, that's completely fine, but you likely need a large team to do so. On the other hand, investing $500M in 20 companies means that you're either writing large first cheques into companies or following on in a meaningful way

Vibes. Just kidding, but not really

As a result, in 2021, the following occurred:

The current allocation to VC in most LP portfolios sat lower than the target as equities and other liquid investments grew in value.

LPs identify the need to deploy more capital than initially expected as per their investment budgeting task

LPs seek out new and existing fund managers to deploy further capital. Here, VCs flexed their mandates on stage and flexed their fund sizes to accommodate the extra interest and any concentration limits that applied. To justify this, VCs spoke about how markets were growing bigger and faster than ever before, and that more talented founders were coming through the pipeline.

Flowing from this, many mega funds popped up, and later-stage investors made seed-stage investments, creating a massive surplus of capital at the early stage.

The Future of VC

In 2023, the aftermath of this is starting to materialise. We have some strong success stories that were funded over the last few years (i.e., Wiz and Deel), but also 3 streams of failed startups.

2019-2020 startups that should've failed in 2021/2022, but secured additional capital to stay alive longer than normal

2021 startups that haven't grown into their valuations, or hit any major milestones to warrant further funding

2021 startups that have plenty of cash left, but no sensible pathway forward - these startups are stuck in a murky middle ground

Because of this, performance for funds from 2019 onwards will likely be lower than normal, unless they've managed to snag a massive winner. However, we will only see these results in 5-7 years’ time once these portfolios have matured.

As a result, there is a good chance that ill-disciplined managers will be able to raise further funds over this period of time. Whilst we're seeing that mega funds are harder to raise, they are still raising substantial amounts of capital. Other fund managers have proactively taken this opportunity to cut their fund sizes in half.

Moreover, there is a lot of dissonance about whether taking venture capital is the right way to build a business as can be seen in the example below:

The most important thing to note here is that using venture capital is only ONE way of building a large business. There are absolutely other ways to build a successful business, and the VC pathway should only be reserved for a specific type of business that is able to deploy the capital effectively.

Unpicking the example above, the story is very similar to a few that I’ve heard over the last few years. Either VCs pushing founders to hire beyond their means or to grow before hitting PMF, the mega fund era of venture capital has literally ruined 100s of legitimate startups due to bad advice and poor incentive alignment.

As a result, VCs currently have a few headwinds in their way:

The barriers to entry for building a business are lower, especially with AI. This also means that the barriers to innovating are lower - we’re seeing this in AI where incumbents are able to spin up their own products quickly and dominate with distribution

Highly negative media stories on a daily basis - WeWork crashing and burning, fraudulent companies getting funding and poor behaviour from VCs are appropriately being flamed in the press all over the world. I hate to see it, but honestly, it was going to happen with the stupid behaviour that was taking place in 2021

Post-COVID, people have largely realised that they should look to enjoy life more, and not push as hard, triggering the Great Resignation. Whilst that’s largely reversed due to cost of living pressures, from a grassroots level, people don’t seem to be willing to push themselves as hard. As a result, people are opting to grow their startups in a more sustainable and leisurely manner that isn’t congruent with receiving investment from a VC

Despite these headwinds, I do still think VC will continue to exist in the long term. As long as institutions remain risk averse with exploring new asset classes or vehicle types and people have big dreams and ambitions, VC as an asset class will remain.

I am clearly biased, but I still truly believe in the ability of VC to create innovation at scale. However, it is a services industry. The service offering needs to be crafted in a way that balances the incentives of large institutional LPs, VC funds and most importantly, the founders that receive investment. Whilst I do have a few thoughts on this, they're better left for a future article.

Make sure to subscribe now to not miss next week’s article

How did you like today’s article? Your feedback helps me make this amazing.

Thanks for reading and see you next time!

Abhi